White-Label Neobank Software Development: A Practical Guide for Marketing Agencies

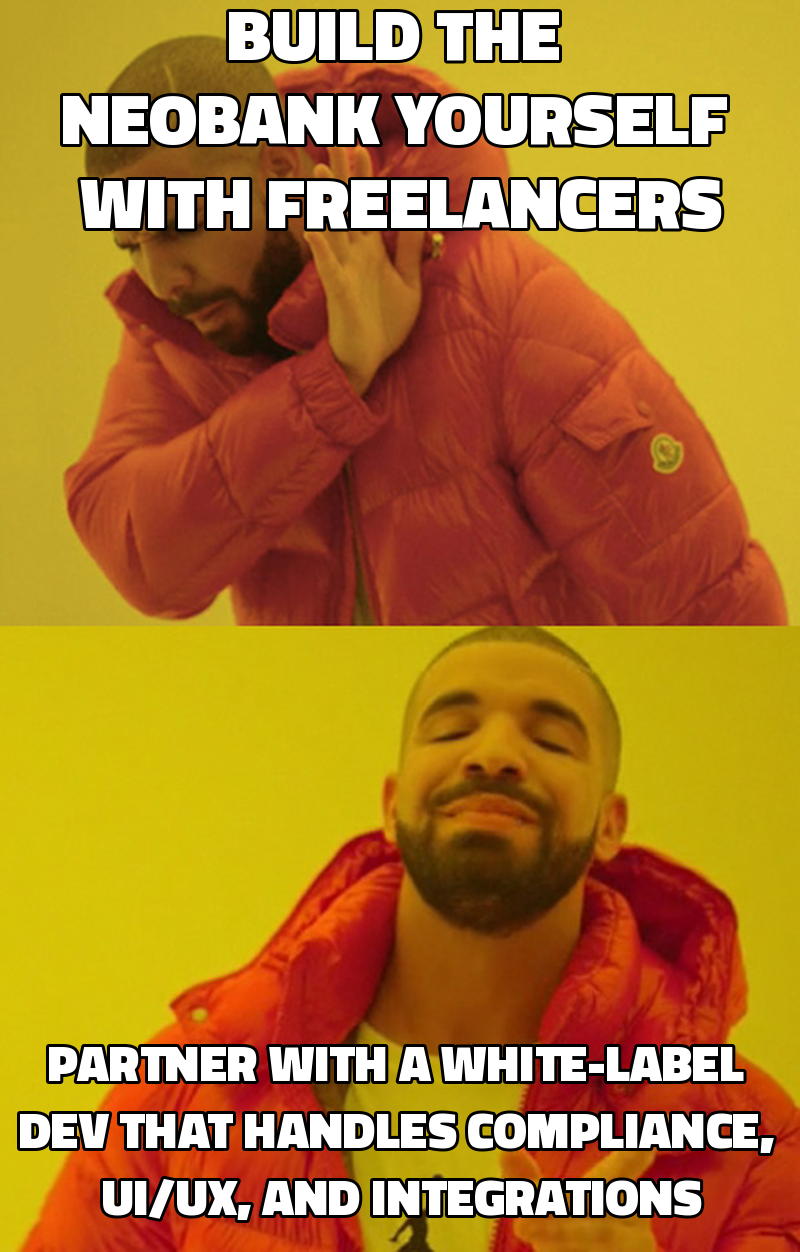

White-label neobank software developers are specialized firms that build fully branded digital banking platforms which agencies can resell under their own name. They handle core banking APIs, compliance layers, and UI/UX design so the agency can focus on client relationships and margin. This guide explains the regulatory, UI/UX, and integration considerations you need before offering a neobank solution to your clients.

Key takeaways

- Choose a partner with a proven compliance framework for the US, UK, and AU to avoid costly licensing delays.

- Insist on a modular UI kit that matches your agency brand guidelines and can be white-labeled without code changes.

- Map every third-party integration (KYC, payments, analytics) to a service-level agreement that defines uptime and data residency.

- Use a fixed-scope pilot (US$2k-5k) to prove delivery speed and then negotiate a retainer for ongoing escalation work.

- Protect your brand with NDA and non-circumvent clauses; the dev partner should remain invisible to the end client.

- Track project status in a shared dashboard to keep client communication transparent and reduce scope creep.

What regulatory hurdles must agencies consider when reselling a white-label neobank?

Regulatory compliance is the single biggest risk for any digital banking product. While the agency does not hold the banking license, the platform it sells must meet the regulator's requirements for the jurisdictions where the end users reside.

| Jurisdiction | Primary regulator | Core licence requirement | Typical KYC/AML standards |

|---|---|---|---|

| United States | Office of the Comptroller of the Currency (OCC) and state banking departments | Federal charter or state charter with a special purpose bank licence | FinCEN Customer Identification Program, OFAC sanctions screening |

| United Kingdom | Financial Conduct Authority (FCA) | Electronic Money Institution (EMI) licence or full banking licence | FCA AML Handbook, UK KYC guidelines, GDPR data protection |

| Australia | Australian Prudential Regulation Authority (APRA) | Authorised Deposit-taking Institution (ADI) or Restricted ADI | AUSTRAC AML/CTF Act, Australian Privacy Principles |

According to a 2023 McKinsey report, 68% of fintech launches in the US fail to meet the full regulatory checklist within the first six months, leading to costly redesigns. Agencies should therefore demand that the white-label partner provides a compliance dossier that includes:

- A copy of the partner's banking licence or charter.

- A documented KYC/AML workflow that maps to the regulator's rulebook.

- Data residency statements confirming where customer data is stored (important for GDPR and Australian Privacy).

- A risk-assessment matrix that shows how the platform handles fraud, chargebacks, and dispute resolution.

By verifying these items up front, the agency avoids the scenario where a client’s launch is delayed because the platform cannot be approved by the regulator.

How can agencies ensure the UI/UX meets both brand standards and banking usability?

A neobank’s success hinges on a frictionless user experience. Agencies that specialize in branding already understand visual identity, but banking adds layers of security, accessibility, and legal wording.

| UI/UX Element | Agency responsibility | White-label partner responsibility |

|---|---|---|

| Visual brand kit (logo, colour, typography) | Provide brand assets and style guide | Apply assets to component library without altering code structure |

| Navigation flow for account opening | Define high-level steps and conversion goals | Build the flow, embed KYC screens, and ensure error handling |

| Accessibility (WCAG 2.1 AA) | Audit final screens for contrast and keyboard navigation | Supply components that already meet WCAG AA standards |

| Security cues (trust badges, encryption icons) | Choose appropriate badge designs | Render badges in the UI and link to security policy pages |

A practical approach is to request a UI component library built in React or Vue that is fully themable via CSS variables. This lets the agency swap colours or fonts without touching JavaScript. The library should also include pre-approved micro-copy for legal disclosures, reducing the need for a separate legal review on each project.

Which integrations are mandatory for a functional neobank and how to manage them?

A white-label neobank is rarely a standalone product. It must connect to at least three core services:

- KYC/Identity verification – providers such as Jumio, Onfido, or Trulioo.

- Payments and card issuance – APIs from Stripe Issuing, Marqeta, or PayPal.

- Core banking ledger – solutions like Mambu, Thought Machine, or Temenos.

Each integration comes with its own SLA, data residency, and cost model. Agencies should create an integration matrix that captures:

- API endpoint URLs

- Authentication method (OAuth2, API key, mutual TLS)

- Expected latency (e.g., <200 ms for card-issuance calls)

- Monthly transaction volume limits

- Pricing tier (per-transaction vs flat fee)

Below is a sample matrix for three common providers.

| Service | Provider | Auth method | Avg latency | Pricing model |

|---|---|---|---|---|

| KYC | Onfido | API key + webhook | 150 ms | US$1 per verification |

| Payments | Stripe Issuing | OAuth2 client credentials | 180 ms | US$0.10 per card + transaction fee |

| Core ledger | Mambu | Mutual TLS | 120 ms | Tiered subscription US$5k-20k per month |

When negotiating with the white-label partner, ask for a single-tenant integration layer that abstracts these providers behind a unified API. This reduces the agency’s technical overhead and makes future provider swaps easier.

How to structure a white-label partnership that protects the agency’s brand and margin?

The partnership model should be simple, repeatable, and legally sound. Below is a step-by-step framework that aligns with the deal shape outlined in the ICP.

- Pilot agreement – A fixed-scope project worth US$2,000-5,000 with a 2-week delivery window. The agency pays the wholesale rate; the partner delivers under the agency’s brand.

- Wholesale pricing sheet – Define the partner’s base cost (e.g., US$1,500 for a standard onboarding flow) and the agency’s markup (typically 50-70%).

- NDA + non-circumvent clause – Both parties sign a mutual NDA. The clause should state that the partner will not contact the agency’s clients directly for a period of 12 months.

- Retainer option – After a successful pilot, the agency can purchase a monthly retainer (US$1,500-2,000) that guarantees 15-20 dev hours for escalation work.

- Shared project dashboard – Use a lightweight tool such as ClickUp or Monday.com with a public view link for the agency’s client. This keeps communication transparent and reduces status-meeting load.

- Escalation path – Define a clear escalation hierarchy (Account manager → Technical lead → Architecture lead) with response time guarantees (e.g., critical issues within 4 hours).

By keeping the partner invisible to the end client, the agency preserves its brand authority while still expanding its service catalogue.

What are the cost implications and ROI expectations for agencies offering white-label neobanks?

Financial modelling shows that a single US$3,000 pilot can generate a US$1,500 gross margin after partner costs. Assuming a conversion rate of 30% from pilot to retainer, an agency that closes three pilots per quarter can realize US$13,500 in gross profit per quarter, or US$54,000 annually.

A 2022 Accenture study of digital banking projects found that agencies that bundled compliance and UI/UX services saw a 2.3× higher client retention rate than those that only offered development. The added value of a turnkey, compliant solution translates into higher lifetime value per client.

How do agencies handle data privacy and security when reselling a neobank platform?

Data privacy is non-negotiable. Agencies must ensure that the white-label partner adheres to the following:

- Encryption at rest and in transit – AES-256 for stored data, TLS 1.2+ for API calls.

- Role-based access control (RBAC) – Only authorized agency staff can view customer PII in the admin console.

- Regular penetration testing – At least annually, performed by a certified third-party (e.g., NCC Group).

- Incident response plan – A documented process that includes notification timelines (72 hours for GDPR breaches).

The agency should request a SOC 2 Type II report from the partner and include a data-processing addendum in the contract that mirrors the agency’s own privacy policy.

Frequently asked questions

How long does it take to launch a white-label neobank for a small business?

A typical end-to-end timeline is 8-12 weeks from signed pilot to live launch. The first 2-4 weeks cover requirements gathering and branding, 3-5 weeks for core integration (KYC, payments, ledger), and the final 2-3 weeks for testing, compliance sign-off, and user acceptance.

Do I need a banking licence to sell a white-label neobank?

No. The white-label partner holds the necessary licence (e.g., EMI in the UK or a federal charter in the US). The agency acts as a reseller and must ensure the partner’s licence is current and covers the jurisdictions of the end users.

What if my client wants a custom feature that the partner does not support?

Because the partner builds on a modular architecture, most custom features can be added as plug-ins. The agency should request a scoped change order with a clear cost estimate before committing to the client.

Can I white-label multiple neobank platforms for different client segments?

Yes, but managing more than two platforms increases integration overhead and brand consistency risk. Most agencies start with a single partner and expand only after establishing a repeatable delivery process.

How do I price the white-label neobank service to stay competitive?

Use a cost-plus model: partner wholesale cost + 50-70% markup. Add a value-added fee for UI/UX customization and compliance consulting. Benchmark against boutique fintech consultancies that charge US$10k-20k for full-stack projects.

What support does the white-label partner provide after launch?

Standard SLAs include 99.9% uptime, 24/7 monitoring, and a 48-hour bug-fix turnaround for non-critical issues. Critical security incidents are usually addressed within 4 hours. Agencies can negotiate extended support as part of the retainer.

Is there a risk of the partner poaching my clients?

A well-drafted non-circumvent clause protects against direct outreach. Additionally, the partner’s branding is hidden in the UI, making it difficult for the client to identify the source.

How can I demonstrate compliance to my clients without being a regulator?

Provide the partner’s compliance dossier, SOC 2 report, and a summary of the KYC/AML workflow. Pair this with a short client-facing compliance checklist that highlights data residency, encryption, and dispute-resolution processes.

white-label

Have something to build?

Tell us what you're trying to ship. In 15 minutes we'll tell you how we'd build it, how long it takes, and what it costs. No pitch deck, no pressure.